GMI x Orange Juice Blog: The Cost of the Dream Report

A Conversation with Jay Anand, Founder, Orange Juice Lab

Interview by Maya Bajaj

1. What motivated Orange Juice Lab to produce The Cost of the Dream?

We spoke to a lot of distributors, labels, artist managers, musicians, and the kinds of clients we work with, and the same gap kept appearing: India had no standard reference point for an artist’s income. The Bass Line Report in Australia was a major influence because it showed what happens when an ecosystem suddenly has a baseline number everyone can use.

Even during my time at GMI, parents would ask, “If my child pursues music, what does that minimum income look like?” And as an industry, we never had a concrete answer. We constantly talk about musicians not earning enough, but we had never put a number to it.

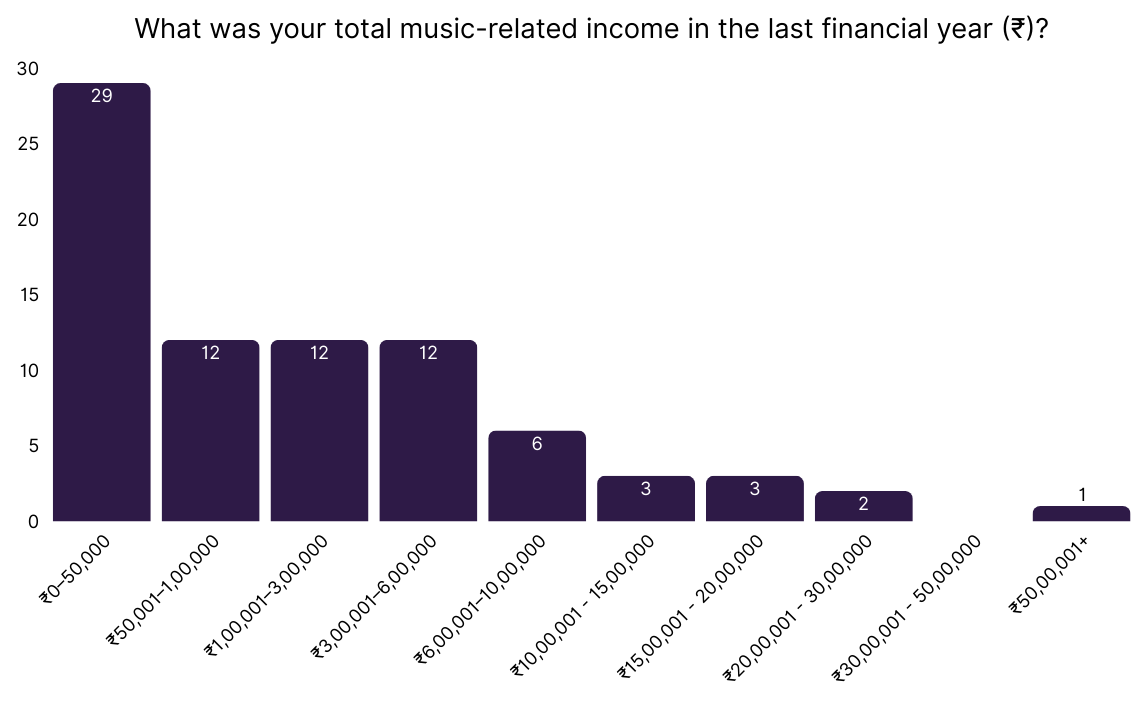

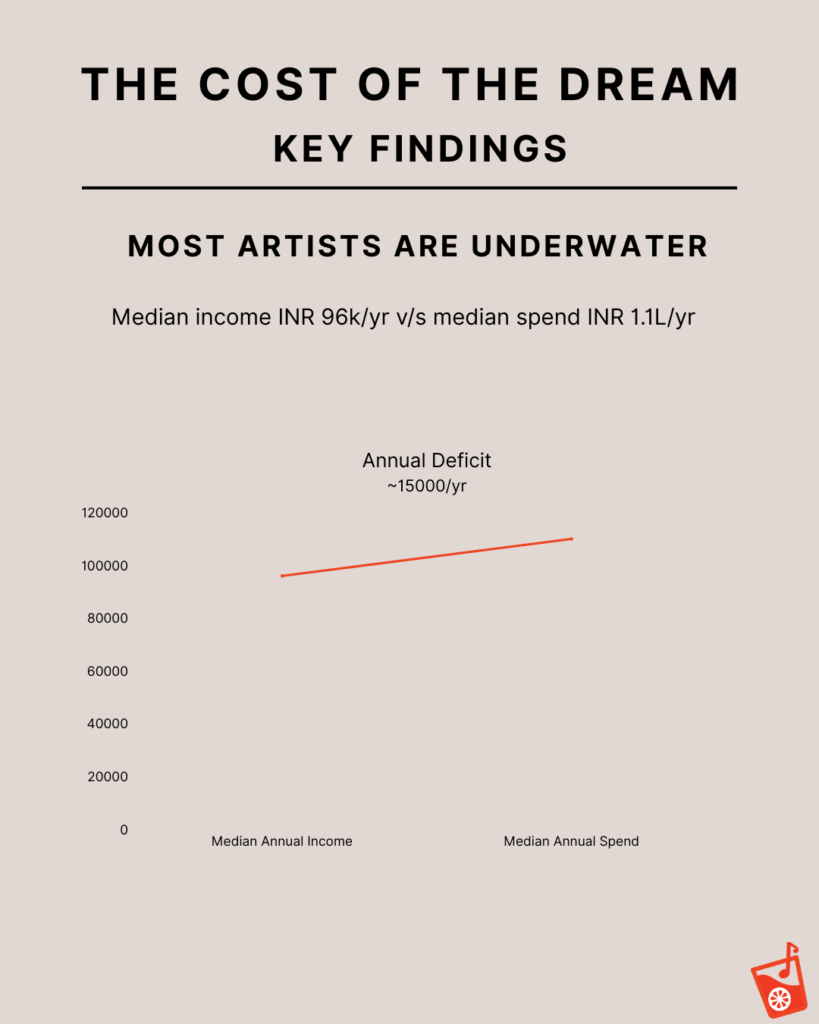

This report was our attempt to finally quantify something everyone intuitively knew. And the numbers were important — for instance, the median annual income of an artist is under ₹1 lakh, while the median annual spend on their career crosses that threshold. That alone was a crucial revelation, because it confirmed that most independent musicians are operating at a net loss before we even consider growth, touring, or experimentation.

So the motivation was twofold:

- highlight this long-standing but unmeasured challenge; and

- understand the parameters around it so the industry can stop speaking abstractly and start speaking accurately.

2. The survey highlights an ecosystem where creative output is high but support structures are thin. From a research perspective, what stood out to you as the most urgent gap that needs attention?

What stood out the most was the contrast between how much artists are creating and how little structural support they actually have. The survey showed incredible diversity — artists creating in 47 genres, 13 languages, and often across multiple formats. Creativity is not the problem.

But when we looked at the barriers, the same two themes came up almost universally:

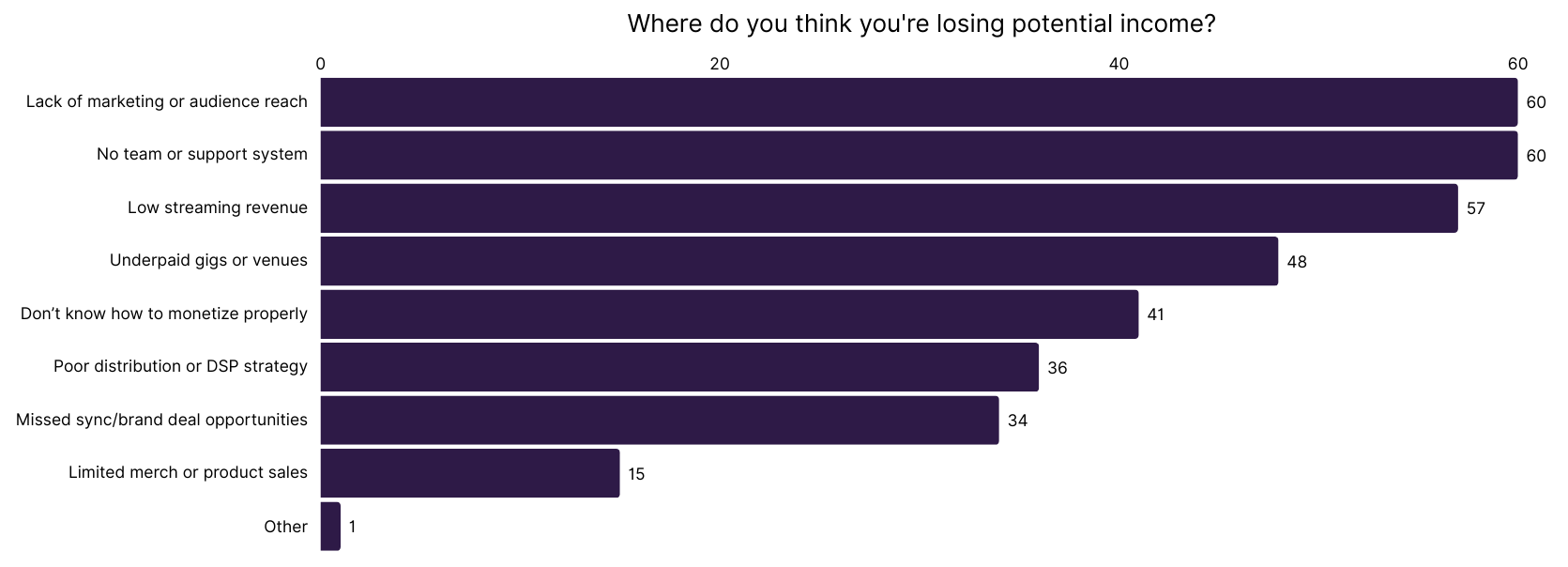

- 75% said they struggle with marketing and reach, and

- 75% said they have no team or support system at all.

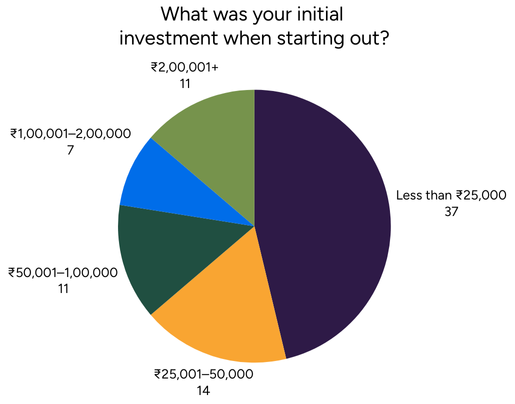

That combination is extremely significant. It means artists are pouring effort into releasing work, but the ecosystem doesn’t give them the scaffolding necessary to turn that effort into income or stability. And because many artists began with extremely modest resources — with almost half starting their career with under ₹25,000 — the lack of support becomes even more limiting.

So the biggest gap isn’t creative output. It’s the absence of the structures that help that output translate into sustainable careers. It’s also important for the artists to understand that they will have to wear multiple hats and build an audience through different means and it cannot be completely offloaded to the industry as a whole to do the job for them.

3. The report points to a “missing middle.” What drives this polarisation, and how does it shape the broader narrative of being an independent musician today?

There are two ways to understand the missing middle.

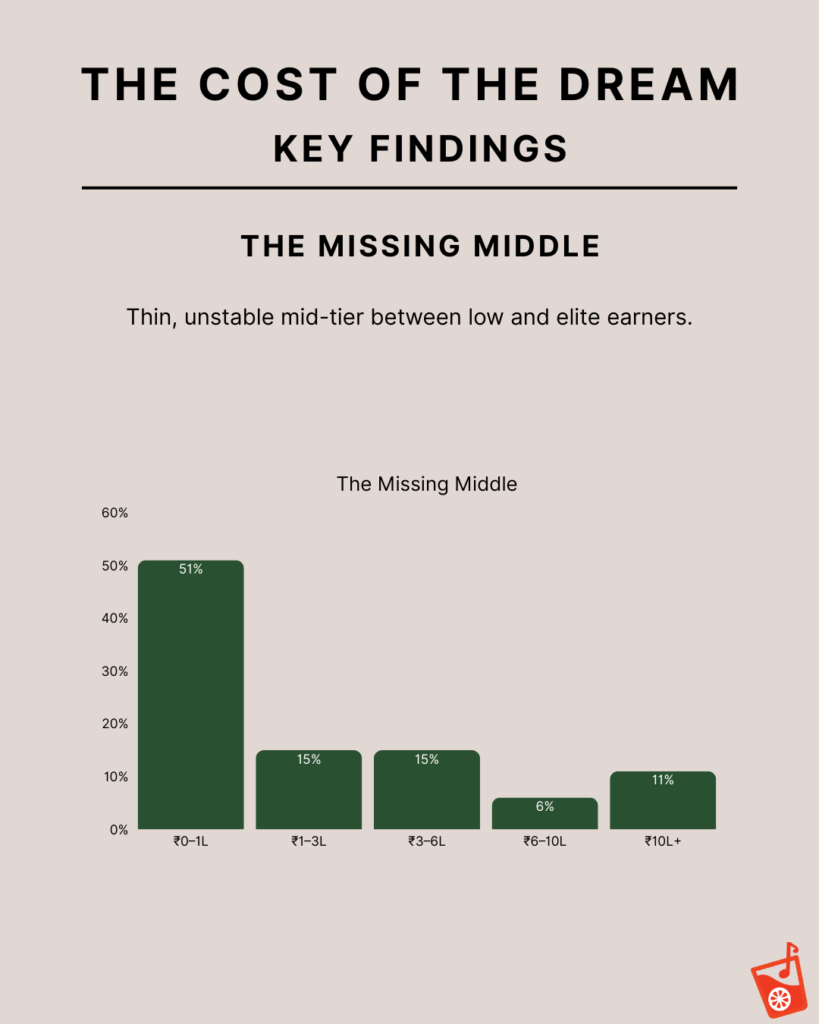

The first is infrastructure. We see plenty of artists who want to move into larger spaces, but India lacks mid-tier venues — the 2,000 to 10,000 capacity range that helps artists transition from club culture to arena culture. Without that ecosystem, the jump becomes extremely slow and extremely expensive. The data reflects this imbalance clearly: the majority of artists cluster at the lower-income end, while only a small percentage cross into higher earning brackets. The “middle” — those in the ₹3–6 lakh or ₹6–10 lakh annual range — is comparatively thin.

The second is audience identification. India is still a young market when it comes to independent live music consumption. A lot of artists reach their mid-career phase still trying to understand who their audience actually is and which cities make sense for them. Without data-driven touring pathways or clarity on regional demand, it’s very difficult for them to build steady momentum.

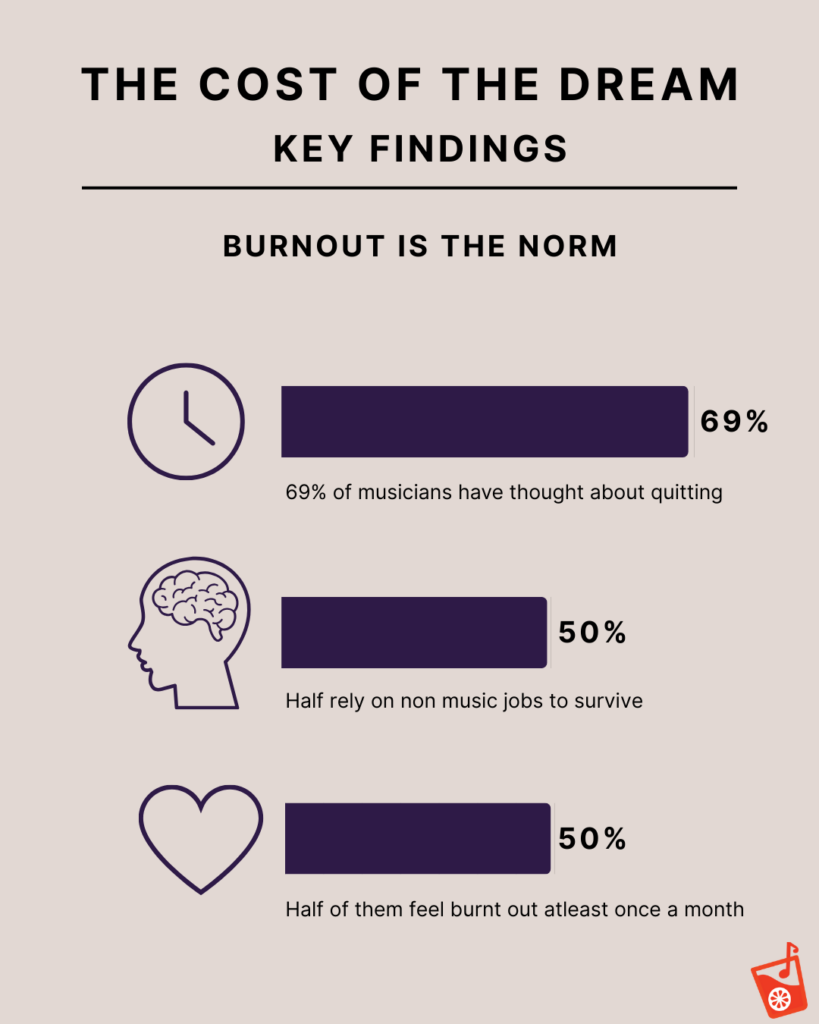

Add to this the economic pressure — with most artists spending more than they earn — and staying in the middle long enough to stabilise becomes nearly impossible. That’s why many end up choosing alternate careers within the ecosystem. It’s not a talent issue; it’s structural.

4. One of the recurring themes was the struggle for consistent stage opportunities. As someone who has been a part of this industry as an artist themselves, what does this tell you about how India’s live music landscape is currently structured?

We weren’t trying to evaluate the live ecosystem directly, but the responses make one thing clear: artists are creating and releasing consistently, but haven’t yet found their audience — and without an audience, venue support becomes limited by default.

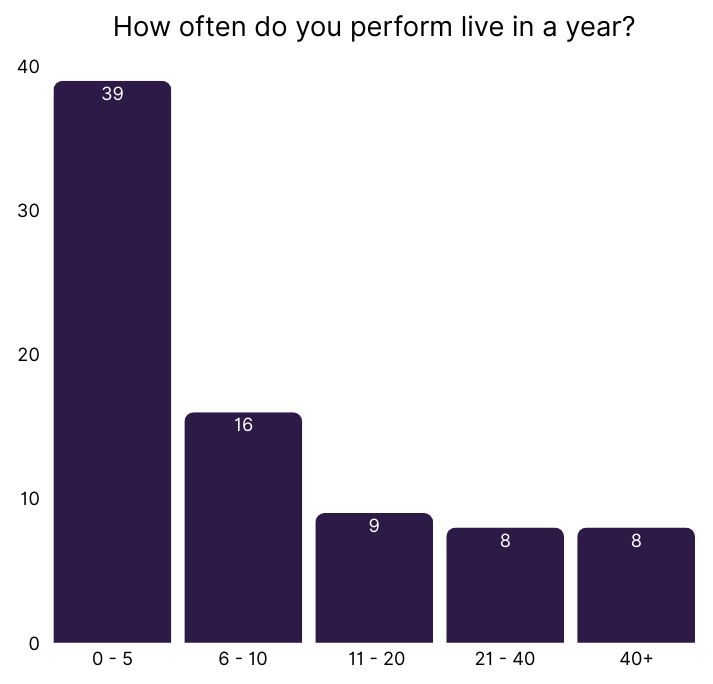

Almost half the artists in the survey perform fewer than five shows a year, even though many have released music for several years. This isn’t because venues don’t want to support new talent; it’s because the demand is not yet visible or predictable. And because artists understandably expect paid gigs, venues need confidence that the audience exists.

This is where the gap in India’s live ecosystem shows up: we need more alternate rooms, small stages, and low-risk spaces where artists can build their audience without the pressure of proving commercial viability immediately. Artists also need to be very strategic — understanding the industry, networking, and identifying where their audience actually is.

The struggle for stage opportunities is less a reflection on artists and more a reflection of how underdeveloped the independent live circuit still is.

5. What lessons could Indian mid-tier cities adopt to retain and support their musicians?

Globally, we’re seeing similar issues — whether in the UK, Australia, or Canada. Even well-developed independent scenes experienced venue closures and market contraction post-pandemic. They may have better infrastructure, but the underlying pressures are shared.

In India, the complexity increases because we don’t have “one” music industry —it’s a collective of multiple micro-markets, each with its own language, culture, and consumption pattern. So a model that works in Sydney, Montreal, or Brighton cannot simply be replicated here.

Mid-tier Indian cities can, however, focus on enabling local ecosystems: creating small cultural hubs, nurturing college circuits, strengthening regional festivals, and investing in community-led spaces. Sustainability comes from context-specific support, not from adopting a one-size-fits-all template.

6. Which income mix do you see as most scalable for an emerging artist?

There’s no single answer because it depends entirely on the artist’s skill set and access. But what we’re seeing — both in the report and in our work — is that a portfolio career is no longer optional.

Teaching, production work, and session opportunities tend to provide early stability. Live shows and streaming contribute to visibility but aren’t predictable income sources at the start. So scalability depends on what the artist is good at and what opportunities they can actually access, not on a predefined formula.

7. Which global practices (micro-grants, transparent gigging networks, touring circuits) could India realistically adapt, and what needs to change locally?

Micro-grants feel like the most immediately implementable solution. Even small grants can help artists produce work they otherwise couldn’t afford. Given that a large portion of artists in our survey self-funded their early careers with under ₹25,000, micro-grants could unlock a lot of creative potential quickly. These could come from government bodies, private organisations, international grant programs, or CSR initiatives.

Touring circuits are also shaping up in India. We’re already seeing renewed interest in live infrastructure — with the resurgence of The Humming Tree in Bangalore and Blue Frog in Mumbai. Transparent gig networks and clear fee structures would help enormously, but they must be adapted to the Indian context rather than copied from other countries.

8. Given the report’s sample (80 artists across 29 cities) and its limitations, how do you plan to scale future editions? How can readers contribute?

This has been our biggest challenge. Because India’s music ecosystem is so fragmented, reaching grassroots communities requires partners who understand their cities and linguistic contexts. And even though the survey is anonymous, artists still hesitate to share financial data — which is understandable.

We’ve seen a positive response to the findings, and that momentum will help. But scaling this requires shared effort. More organisations and communities need to see the value in having this data publicly accessible. We begin tracking the next edition after the financial year closes — from April 1st 2026, covering FY 2025–26 — and we hope more partners will help us reach new regions.

Anyone who wants to share data, host collection points, or collaborate is welcome to reach out. The doors are always open.

9. If this study could catalyse one structural change in the independent music ecosystem, what would you hope it to be?

Two shifts, both connected:

First, I hope artists start finding opportunities in front of the right audiences. The biggest unlock for an emerging musician is understanding where their listeners actually are and choosing opportunities aligned with that.

Second, I hope we see more alternative spaces — beyond social media and beyond high-pressure, ticketed shows — where artists can perform, experiment, and grow their audience.

If someone is building something in this direction, we would love to hear from them. One of our intentions with this report is also to track ideas and innovations that emerge from it.

Read the full report, The Cost of the Dream: Mapping the Realities of Non Film Musicians in India

About Orange Juice Lab

![]()

Orange Juice Lab came out of my own lived experience of moving through the music ecosystem in many different roles. I started as a working musician and educator, teaching students across age groups and contexts, while also trying to build a sustainable career for myself. Over time, that path led me into curriculum design, partnerships, product thinking, and eventually working closely with institutions, artists, and industry stakeholders.

Across all these roles, I kept encountering the same friction points: artists unsure how to navigate the business side of music, institutions struggling to keep pace with a rapidly changing industry, and companies entering the Indian market without a clear understanding of its cultural and structural realities. There was no shortage of ambition or talent, but there was a shortage of frameworks, data, and shared language to make informed decisions.

Orange Juice Lab was created as a way to bridge those gaps. It’s not a consultancy in the traditional sense, but an R&D lab focused on building data-backed insights, educational programs, and development frameworks that are rooted in real-world experience. The intent is to create systems that help people make better decisions, whether they’re artists shaping sustainable careers, or organisations trying to build future-ready strategies in music.

At its heart, Orange Juice Lab reflects my belief that the music industry doesn’t need more noise, it needs clearer thinking, stronger infrastructure, and spaces where learning, experimentation, and long-term impact can coexist.